#Life

Can India’s Financial System Make Room For Faith?

India, with over 200 million Muslims, hosts the third-largest Muslim population globally. Despite this, the country’s banking system has largely failed to cater to the community’s specific financial needs. This exclusion isn’t due to a lack of access or equal opportunity, but stems from significant theological differences between Islamic finance principles and the conventional banking system.

Socio-Economic Disparities

The Sachar Committee Report (2006) highlighted the socio-economic backwardness of Muslims in India. Despite constituting about 14% of the population, Muslims held only 7.4% of bank deposits and received just 4.7% of bank credit. This disparity limits their ability to access institutional credit for significant endeavors, such as starting businesses or pursuing higher education, thereby affecting their representation in business and wealth accumulation.

A 2015 analysis by the ET Intelligence Group of the BSE 500 companies further revealed that Muslim representation in director and top executive positions was a mere 2.67%, indicating a significant underrepresentation in corporate leadership.

Keep supporting MuslimMatters for the sake of Allah

Alhamdulillah, we're at over 850 supporters. Help us get to 900 supporters this month. All it takes is a small gift from a reader like you to keep us going, for just $2 / month.

The Prophet (SAW) has taught us the best of deeds are those that done consistently, even if they are small. Click here to support MuslimMatters with a monthly donation of $2 per month. Set it and collect blessings from Allah (swt) for the khayr you're supporting without thinking about it.

Further, Muslims hold only 9.2% of gold assets, compared to 31% held by Hindu high castes and 39% by OBCs, highlighting their limited access to collateral for financial transactions.

Theological Foundations of Islamic Finance

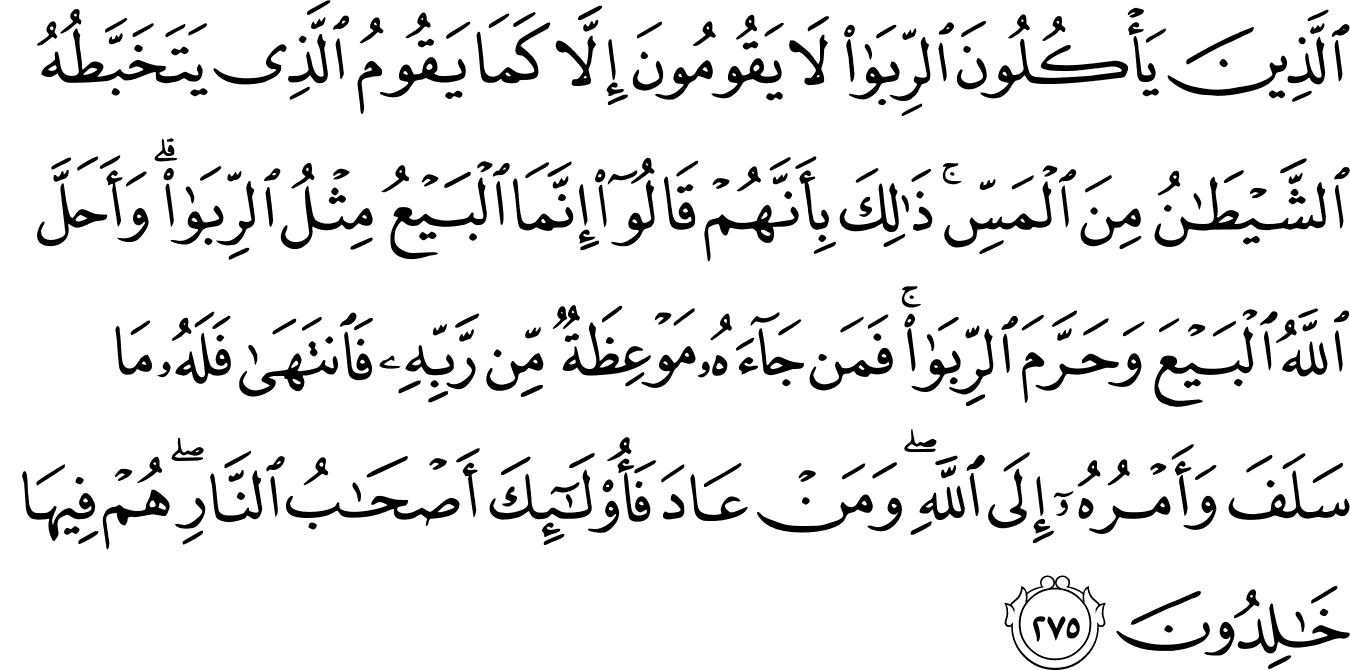

Islamic finance is grounded in principles that promote justice, welfare, and ethical economic practices. Central to these principles is the prohibition of ‘riba’ (interest), as it is considered exploitative and unjust.

“Those who consume interest cannot stand [on the Day of Resurrection] except as one stands who is being beaten by Satan into insanity. That is because they say, “Trade is [just] like interest.” But Allah has permitted trade and has forbidden interest. So whoever has received an admonition from his Lord and desists may have what is past, and his affair rests with Allah. But whoever returns to [dealing in interest or usury] – those are the companions of the Fire; they will abide eternally therein.” [Surah Al-Baqarah: 2;275]

“O you who have believed, do not consume usury, doubled and multiplied, but fear Allah that you may be successful.” [Surah ‘Ali-Imran: 3;130]

Instead, Islamic finance encourages (1) asset-backed transactions:

Narrated by Hakim b. Hizam ") : “I asked Messenger of Allah

: “I asked Messenger of Allah ") , I said: ‘A man came to me asking to buy something that I did not have. Can I buy it from the market for him and then give it to him?’ He said: ‘Do not sell what is not with you.'” [Jami` at-Tirmidhi 1232]

, I said: ‘A man came to me asking to buy something that I did not have. Can I buy it from the market for him and then give it to him?’ He said: ‘Do not sell what is not with you.'” [Jami` at-Tirmidhi 1232]

(2) profit and loss sharing:

Narrated ‘Urwah Al-Bariqi: “The Messenger of Allah gave me on Dinar to purchase a sheep for him. So I purchased two sheeps for him, and I sold one of them for a Dinar. So I returned with the sheep and the Dinar to the Prophet , and I mentioned what had happened and he said: ‘May Allah bless you in your business dealings.’ After that we went to Kunasah in Al-Kufah, and he made tremendous profits. He was among the wealthiest of the people in Al-Kufah.” [Jami` at-Tirmidhi 1258],

Wealth in Islam is viewed as a means to promote circulation and mutual support,

Abu Huraira reported Allah’s Messenger ﷺ as saying: “Charity does not decrease wealth, no one forgives another except that Allah increases his honor, and no one humbles himself for the sake of Allah except that Allah raises his status.” [Sahih Muslim: 2588]

and not as a commodity to be hoarded.

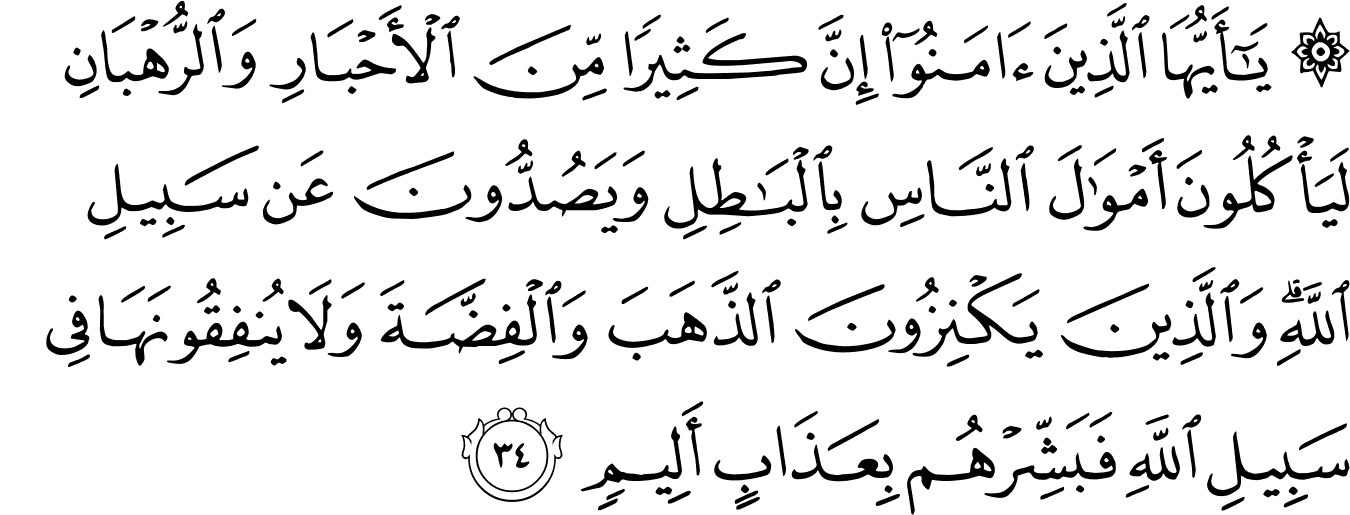

“O you who have believed, indeed many of the scholars and the monks devour the wealth of people unjustly and avert [them] from the way of Allah. And those who hoard gold and silver and spend it not in the way of Allah – give them tidings of a painful punishment.” [Surah at-Tawbah; 9:34]

This approach aims to reduce economic disparities and promote a more equitable society:

Abu Wa’il narrated that Qais bin Abi Gharazah said:

“The Messenger of Allah

came to us, and we were what was called ‘brokers,’ he said: ‘O people of trade! Indeed the Shaitan and sin are present in the sale, so mix your sales with charity.'”He said: There are narrations on this topic from Al-Bara’ bin ‘Azib and Rifa’ah.

[Abu ‘Eisa said:] The Hadith of Qais bin Abi Gharazah (a narrator) is a Hasan Sahih Hadith.

Mansur, Al-A’mash, Habib bin Abi Thabit, and others reported it from Abu Wa’il, from Qais bin Abi Gharzah, from the Prophet ﷺ. We do not know of anything from the Prophet ﷺ narrated by Qais other than this. [Jami` at-Tirmidhi 1208]

Legal and Institutional Challenges

The Banking Regulation Act, 1949, forms the backbone of India’s banking system, which is predominantly interest-based. This framework presents challenges for integrating Islamic finance, which operates on principles contrary to interest-based lending.

Various committees have examined the feasibility of Islamic banking in India. The Anand Sinha Committee (2005) deemed it incompatible within the existing legal framework, while the Raghuram Rajan Committee (2008) acknowledged that interest-free banking could provide financial access to excluded communities. However, in 2017, the proposal for Islamic banking was rejected, citing the need for equal opportunities for all citizens.

International Models and Secularism Concerns

Countries like the UK and Germany have implemented faith-based banking models, providing services that align with Islamic principles. Similarly, Muslim-majority nations such as Malaysia and Indonesia have successfully integrated Islamic banks alongside conventional ones, demonstrating that dual systems can coexist.

Critics argue that introducing Islamic banking in India could challenge secularism by creating a parallel economy. However, India already accommodates religious diversity in its economic and legal systems—such as Hindu Undivided Family (HUF) accounts enjoying tax benefits and the operation of Muslim personal law and waqf boards. Therefore, allowing financial models that address the ethical concerns of Muslims may enhance substantive equality without undermining secularism.

Potential Solutions: NBFCs and Cooperative Models

Establishing full-fledged Islamic banks in India faces significant legal and political challenges. However, Non-Banking Financial Companies (NBFCs) offer a viable alternative. Since NBFCs are not governed by the Banking Regulation Act, they can operate with asset-backed transactions in line with Islamic finance principles. An example is Cheraman Financial Services in Kerala, approved by the Reserve Bank of India in 2013, which provides interest-free financial services.1https://prsindia.org/files/policy/policy_committee_reports/1242304423–Summary%20of%20Sachar%20Committee%20Report.pdf

Additionally, cooperative models and Islamic banking windows within existing institutions can provide services that align with Islamic principles, fostering economic inclusion and narrowing the participation gap between the Muslim community and others.

Conclusion

The debate on Islamic banking in India underscores a broader tension between a uniform legal framework and the need for economic inclusion of minorities. While establishing full-fledged Islamic banks may be legally and politically challenging, NBFCs, cooperative models, and Islamic banking windows within existing institutions offer feasible alternatives. What is needed is not rejection but regulatory innovation—approaches that can reconcile India’s secular commitments with the financial participation of one of its largest minority communities.

Related:

– Perpetual Outsiders: Accounts Of The History Of Islam In The Indian Subcontinent

– Meaningful Money: How Financial Literacy Amplifies Your Giving

Keep supporting MuslimMatters for the sake of Allah

Alhamdulillah, we're at over 850 supporters. Help us get to 900 supporters this month. All it takes is a small gift from a reader like you to keep us going, for just $2 / month.

The Prophet (SAW) has taught us the best of deeds are those that done consistently, even if they are small. Click here to support MuslimMatters with a monthly donation of $2 per month. Set it and collect blessings from Allah (swt) for the khayr you're supporting without thinking about it.

The Arithmetic Of Longing: On Loneliness, Desire, And Learning To Want Well

Far Away [Part 20] – Among the Afghans

The Legacy Of Professor John Esposito: The Scholar Who Refused To Turn Islam Into An Enemy

Tahajjud: A Call to All Pajama Heroes

Thinking Long-Term: The Legacy of Yahiya Emerick

When Tawakkul Isn’t Enough: Why Financial Silence Hurts Marriages

Thinking Long-Term: The Legacy of Yahiya Emerick

The Arithmetic Of Longing: On Loneliness, Desire, And Learning To Want Well

The Legacy Of Professor John Esposito: The Scholar Who Refused To Turn Islam Into An Enemy

An Inconvenient American in Syria: The Curious Case of Bilal Abdul-Kareem

The Best Actions for Eid al-Adha [Imam Dawud Walid]

Coming Full Circle: Who Are You Now? | Night 30 with the Qur’an

Running Away From Who We Are | Night 29 with the Qur’an

Building From the Ground Up: Week 4 Recap | Night 28 with the Qur’an

The Muslim You Are Becoming | Night 27 with the Qur’an

-

#Life1 month ago

#Life1 month agoOn Infertility And Not Having A Child: A Letter To Couples Going Through The Silent Struggle

-

#Islam1 month ago

The Woman Who Corrected Umar: Mahr, Tafseer, and Advocacy

-

#Life1 month ago

So You Want To Become A Lawyer? [Part I] – On Faith, Duty, And The Legal Profession

-

#Culture1 month ago

Far Away [Part 17] – The Caravan